How profitable is my business?

At the start of a new year what better time to make sure you’re going to track the right metrics and get a better understanding of your figures.

You’re probably now thinking “really?” after reading that but it’s true. You can’t ignore your numbers and the biggest number of all is your profit.

Your profit IS your business. That’s where the business actually lies because without it you’re just playing shop I’m sorry to say.

I’ve written a lot recently about cash flow and the main reason it’s caused is because your profit falls short of where it needs to be.

So let’s focus on profit - I’m going to take you through what to consider when calculating it. This is a whistle stop tour but it covers all the main areas.

But before I begin, if you don’t already I would have a P&L (Profit & Loss sheet) active within your business that you check in on every week. It really does make a huge difference and it’s the only way you can get a read on the efficiency of your business cash wise.

Here goes…

So what is your profit?

Your profit is what’s left when all costs are considered. It’s the actual money made when all is said and done.

It’s what we refer to as your net profit % or just net profit. You can also look at it before tax (your operating profit) or post profit.

What I’m referring to here is your absolute net profit, everything in minus every out. The absolute bottom line/net income.

It’s easy to look at the balance in your business bank account and think, “Great, that’s mine to spend!” But, there’s much more to it than that. That number doesn’t tell you the full picture of your business’s financial health. And, it’s certainly not yours to spend (hello, no.1 business owner fail).

Before you start planning how to use that money, you need to calculate your actual profit. This means understanding all the costs that eat into your revenue each month - made up of fixed and variable costs.

Here’s a breakdown of what to consider when working out your profit.

1. Cost of Goods Sold (COGS)

This includes the direct costs of producing or purchasing your products - it’s basically any cost associated with the actual product including:

The wholesale price or manufacturing cost of your items - basically what you bought it for.

Materials or components needed to create the product if you’re the one doing the ‘making’.

The landed cost - what this means is the shipping/duty/tax/container costs you pay to get the product to you.

Any packaging applied to the direct product.

2. Shipping and Delivery Costs

This is something often forgotten about, don’t make this mistake. It includes the cost of the shipping to you as a business and also the shipping revenue that comes in from the customer. The difference is what you should be focussing on.

Firstly, your cost as a business - include in this postage costs and packaging materials like boxes, tape, inserts etc. You shouldn’t really try to make money from P&P but you should attempt to have your costs covered. Businesses will often absorb some of the shipping costs themselves but this is often made up for in the product costs.

Check the difference between your cost and the cost to the customer overall each month. Bear in mind that any free shipping you offer could skew this too.

3.Storage and Warehousing

If you hold stock is there a cost to this? If you use fulfilment, have a unit, warehouse etc then make sure you include this cost.

4.Marketing and Advertising

Think about your spending on ads and any influencer collaborations for example. These costs support sales but need to be deducted when calculating your net profit.

5.Website, App charges & payment fees

Don’t forget about platform fees (Shopify, Etsy, etc.), and payment processing fees (PayPal, Stripe, Klarna etc.) - these are often overlooked but they really can rack up.

6.Software Subscriptions

Accounting software, inventory management tools, your email marketing platform? These monthly or annual subscriptions are part of your business costs too. Go through your business bank account and make sure you understand exactly what you’re paying.

7.Packaging and Branding Materials

Think about the costs of custom labels, branded boxes, or thank you cards. These enhance the customer experience but need to be included in your expenses - again another thing that can be totally overlooked.

Don’t confuse this with the cost of your direct packaging to your products (if this applies to you) such as wholesale boxing etc. This is the packing you add to dispatch an order, that’s the best way to think about it.

8.Team or Outsourcing Costs

If you have employees, contractors, or freelancers, their wages, benefits, or fees are a significant part of your costs. Even small outsourcing tasks, like hiring a designer or photographer, count here. Don’t miss any of these out.

9.Utilities and Overheads

Don’t forget everyday running costs like electricity, internet, or rent for office or production space.I generally don’t include this if you’re working from home unless the size of your operation from home is significant.

10.Taxes and VAT

Depending on your turnover, you’ll need to set aside money for taxes and VAT. These obligations can vary but are non negotiable expenses. The best way to account for these is to put them aside monthly and know exactly what % you’re removing from your overall revenue for them. I always advise a bank account such as Starling that allows you to create ‘pots’ where you can assign money for any commitments such as these.

11.Returns, Refunds & Waste

Some customers will return products, and refunds eat into your revenue. It’s wise to account for this in your profit calculations. Have a look at what % this is each month for your business and apply this. If you also think that ‘waste’ is significant enough to record then also apply this - it could be 0.5-1% a month.

What’s normal?

One thing to note about a P&L - it’s not what’s in your bank as your balance. It’s an assessment of how profitable your business runs, how efficient it is financially and it’s certainly what someone would want to know if you ever wanted to sell it.

It’s normal to see higher costs during certain times of the year like when you’re stocking up for busy seasons or launching a new collection. It’s also normal for profit margins to vary by product. Some items may be “loss leaders,” generating less profit but driving customer interest in higher margin products in the long term. There’s also seasons and events to consider.

All of that is fine as long as over a 12 month period it balances out.

A healthy bottom line can range between 10-20% for a business that pays VAT and tax. You might see a higher net margin if you don’t pay either or both of these.

The first starting block when it comes to costs is your product margin - get this wrong and you can see how your margin can easily be eroded. Some considerations:

Re-sellers will generally sell at lower margins with more of an emphasis on volume.

Depending on your business set up you may incur higher business/running costs.

Some advice

Don’t base your figures around anyone else’s business, each business is different and each has its nuances. Some will have much lower costs than yours and vice versa.

Know what your break even amount is each month and then you’ll know at what point within the month you’ve hit it. For example, you could typically see your business costs accounted for within the first 2 weeks.

The more you ‘overcome’ your business costs, the greater your net profit will be.

Some months there is much more opportunity to drive net profit (usually around events and seasonal and/or new product launches) - when this is the case push hard.

It’s much easier to push harder in your peaks than focusing on bringing the overall revenue up each month - take full advantage of these times.

Make sure you undertake a thorough cost cutting exercise annually at least to make sure you’re not losing any profit in this way.

Why you should focus on profit

Looking at your business in this way forces you to understand all the costs that go into running your business which will give you a clearer view of your actual earnings. It allows you to make smarter decisions about reinvesting in your business, paying yourself, or saving for the future.

And hopefully it curbs your spending preventing any cash flow issues!

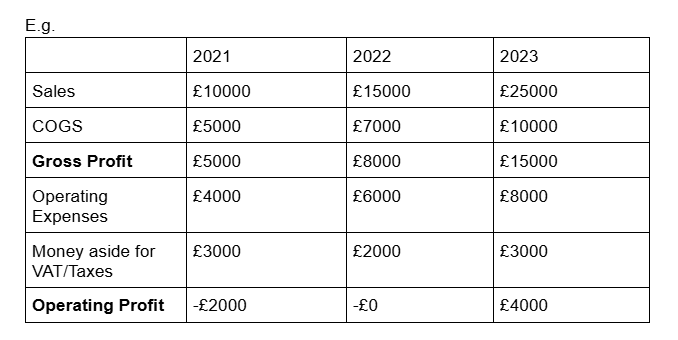

How to Calculate Monthly Profit

Start with Revenue: Add up all your sales for the month.

Subtract COGS: This gives you your gross profit.

Deduct Operating Expenses: Include all the costs listed above (marketing, storage, shipping, etc.).

Account for Taxes: Set aside money for income tax, VAT, or other obligations.

The Result? Your Net Profit: This is the amount your business truly earned after covering all costs.

Your bank balance doesn’t equal profit—it’s just a starting point. By understanding all the costs that go into running your business, you’ll have a clearer view of your actual earnings. With this knowledge, you can make smarter decisions about reinvesting in your business, paying yourself, or saving for the future.

Remember, profit is the reward for all your hard work—so take the time to calculate it right!